Backtest Example¶

This example executes a backtest of the Strategy Example against BTC data. For details regarding how figures were generated see the Plot Backtest routine.

Python source code: ../../examples/backtest.py

import boatwright

from MACD import MACD

from boatwright.PerformanceMetrics import ROI, PercentProfit, SharpeRatio

from boatwright.Data.OHLCV.CSVdatabase import CSVdatabase

from datetime import datetime

import matplotlib.pyplot as plt

# 1. define the backtest broker model

broker = boatwright.Brokers.BacktestBroker(starting_aum=10000, taker_fee=0.1, maker_fee=0.1, slippage=0, quote_symbol="USD")

# 2. define the strategy

strategy = MACD(fast_period=7, slow_period=14, symbol="BTC")

# 3. load data for the backtet (including prequisite data for necessary for signal generation)

database = CSVdatabase(source="ALPACA", debug=False, dir="./quickstart_data")

data = database.load(

symbol=strategy.symbol,

start=datetime(year=2025, month=2, day=1, hour=0, minute=0),

end=datetime(year=2025, month=12, day=31, hour=0, minute=0),

prerequisite_data_length=strategy.calc_prerequisite_data_length(),

granularity=1, granularity_unit="DAY",

verbose=True

)

print(data)

# 4. declare and run the backtest

backtest = boatwright.Backtest(strategy=strategy, data=data, broker=broker, debug=False)

backtest.run(verbose=True)

# 5. analyze results

print(f"ROI: {ROI().calculate(backtest)}")

print(f"Percent Profit: {PercentProfit().calculate(backtest)}")

print(f"Sharpe Ratio: {SharpeRatio().calculate(backtest, risk_free_rate=0, increments_per_year=365*24*60)}")

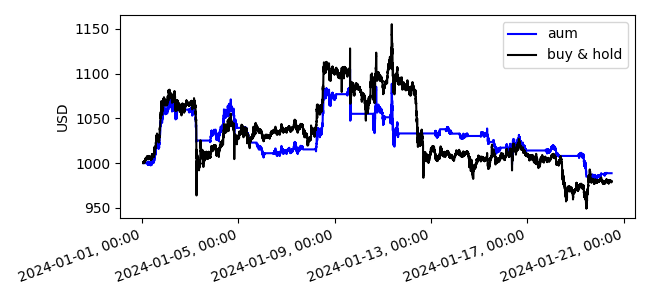

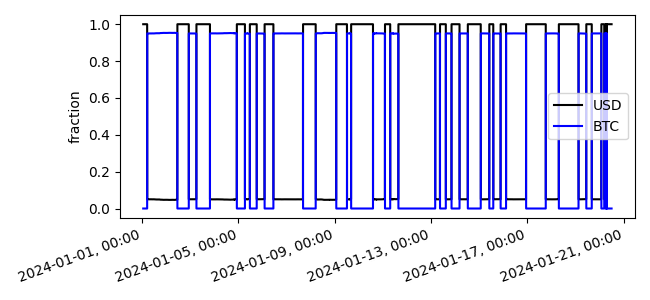

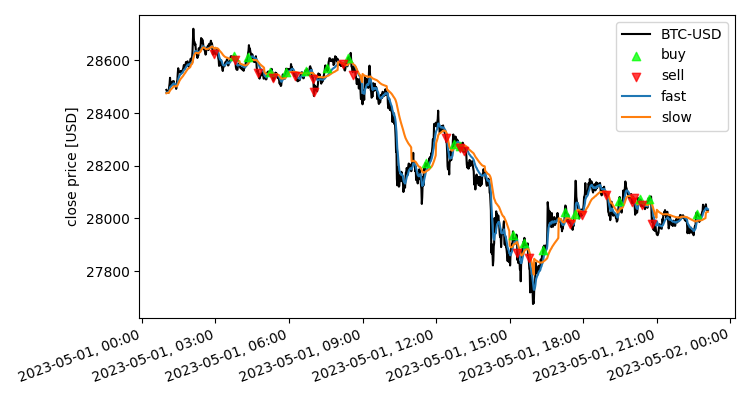

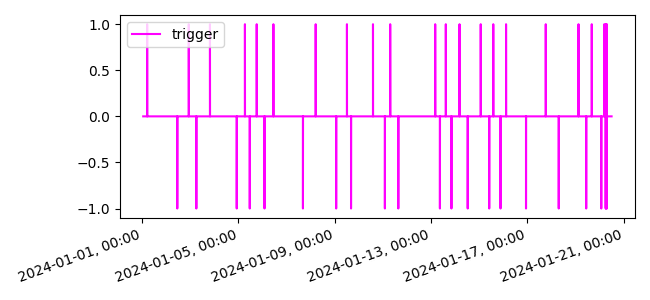

figs, axs = boatwright.Visualization.plot_backtest(backtest, candles=True)

# saving figures for documentation

figs["aum"].savefig("../docs/examples/images/backtest/aum.png")

figs["assets"].savefig("../docs/examples/images/backtest/asset_fraction.png")

figs["price"].savefig("../docs/examples/images/backtest/close.png")

figs["trigger"].savefig("../docs/examples/images/backtest/trigger.png")

plt.show()